Bank of Mom & Dad: Smart Strategy or Risky Business?

A simple graphic has been making the rounds lately:

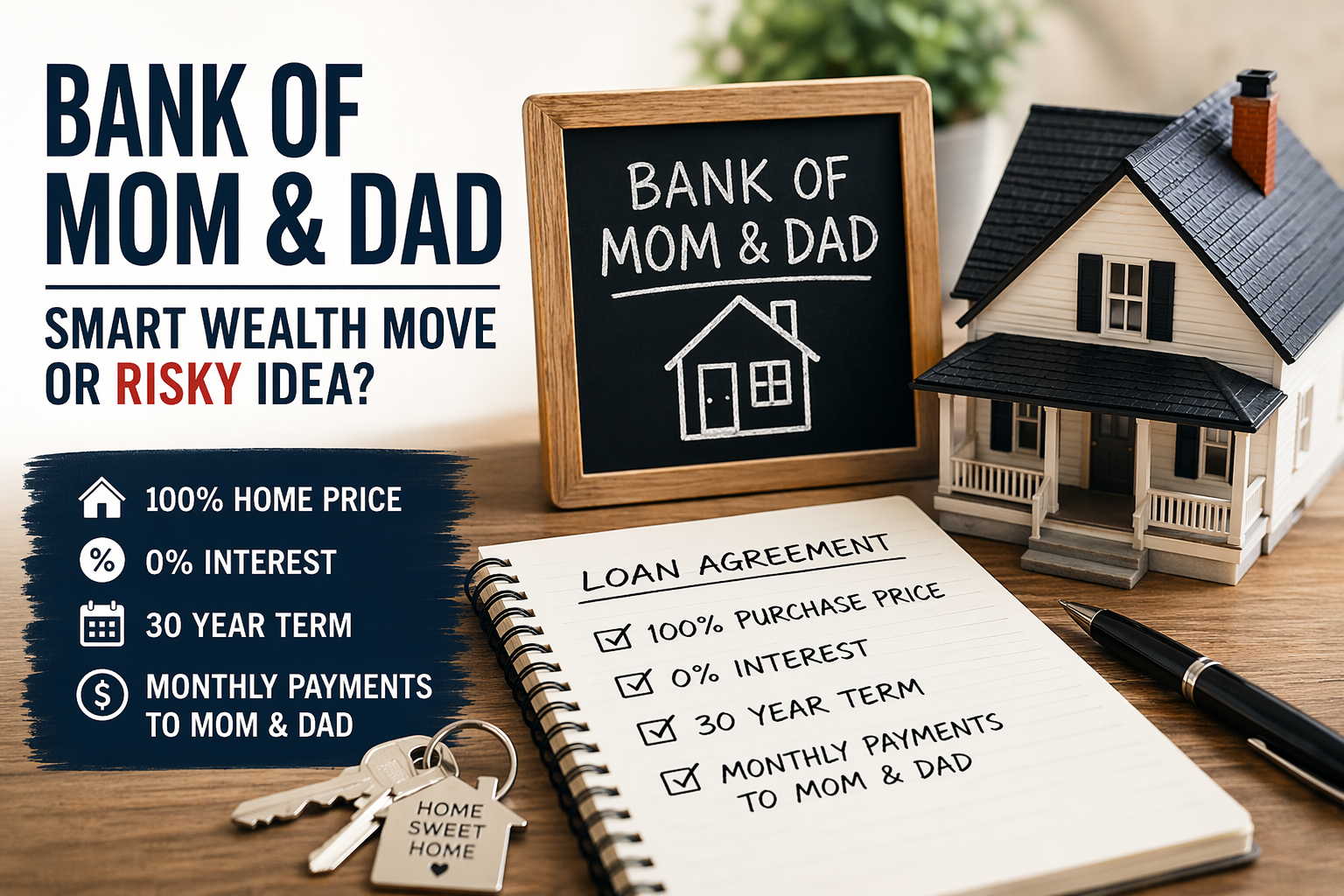

A parent offers to finance their child’s home purchase—100% of the price, 0% interest, paid back over 30 years.

At first glance, it sounds almost absurd. Zero interest? No bank? No underwriting headaches?

But take a step back and compare it to the traditional system, and suddenly it doesn’t seem so far-fetched.

Why the Idea Is So Appealing

If a family has the financial strength to pull it off responsibly, the benefits are hard to ignore.

Instead of paying hundreds of thousands of dollars in interest to a lender, that money stays within the family. Monthly payments don’t disappear into a bank’s balance sheet—they become a tool for building generational wealth.

It also creates an opportunity to:

Help a child get into a home sooner

Lock in stable, predictable payments

Keep assets and equity within the family long-term

In a housing market where affordability has become one of the biggest barriers for first-time buyers, it’s easy to see why this idea resonates.

The Reality Check

Of course, what works on paper doesn’t always work in real life.

The moment you remove the bank, you also remove a neutral third party. That’s where things can get complicated.

Some very real questions come into play:

What happens if payments are late—or stop altogether?

How do you handle disagreements without damaging the relationship?

Does financial support encourage responsibility… or delay it?

Money has a way of amplifying emotions, and even the strongest families aren’t immune to tension when large sums are involved.

Why This Conversation Is Happening Now

Ideas like this aren’t gaining traction in a vacuum.

Home prices have risen dramatically over the past several years, while interest rates have made borrowing more expensive. For many young buyers, the traditional path to homeownership feels increasingly out of reach.

So families are getting creative.

Whether it’s co-signing, gifting down payments, or exploring private financing arrangements like this one, parents are stepping in more than ever before.

Is There a Middle Ground?

For some families, a structured approach can help reduce risk:

Put everything in writing (just like a traditional mortgage)

Set clear expectations for payments and consequences

Consider involving an attorney or title company

Treat it like a business transaction—because it is one

Done right, it can function very similarly to a bank loan—just without the interest.

Done poorly, it can strain relationships in ways that are hard to repair.

So… Smart Move or Messy Idea?

The truth is, it depends entirely on the family.

For disciplined households with clear communication and strong financial footing, this can be a powerful wealth-building strategy.

For others, it may introduce more risk than reward.

What’s undeniable is this: the fact that more people are seriously considering ideas like this says a lot about today’s housing market.

What do you think?

Is the “Bank of Mom & Dad” a smart way to build family wealth…

or one of those ideas that sounds better in theory than in real life?