The Mortgage Industry Has Trained Buyers to Ask the Wrong Question

"What's your interest rate?"

It's one of the first questions almost every homebuyer asks.

And while it's an understandable question...

...it may also be the wrong one.

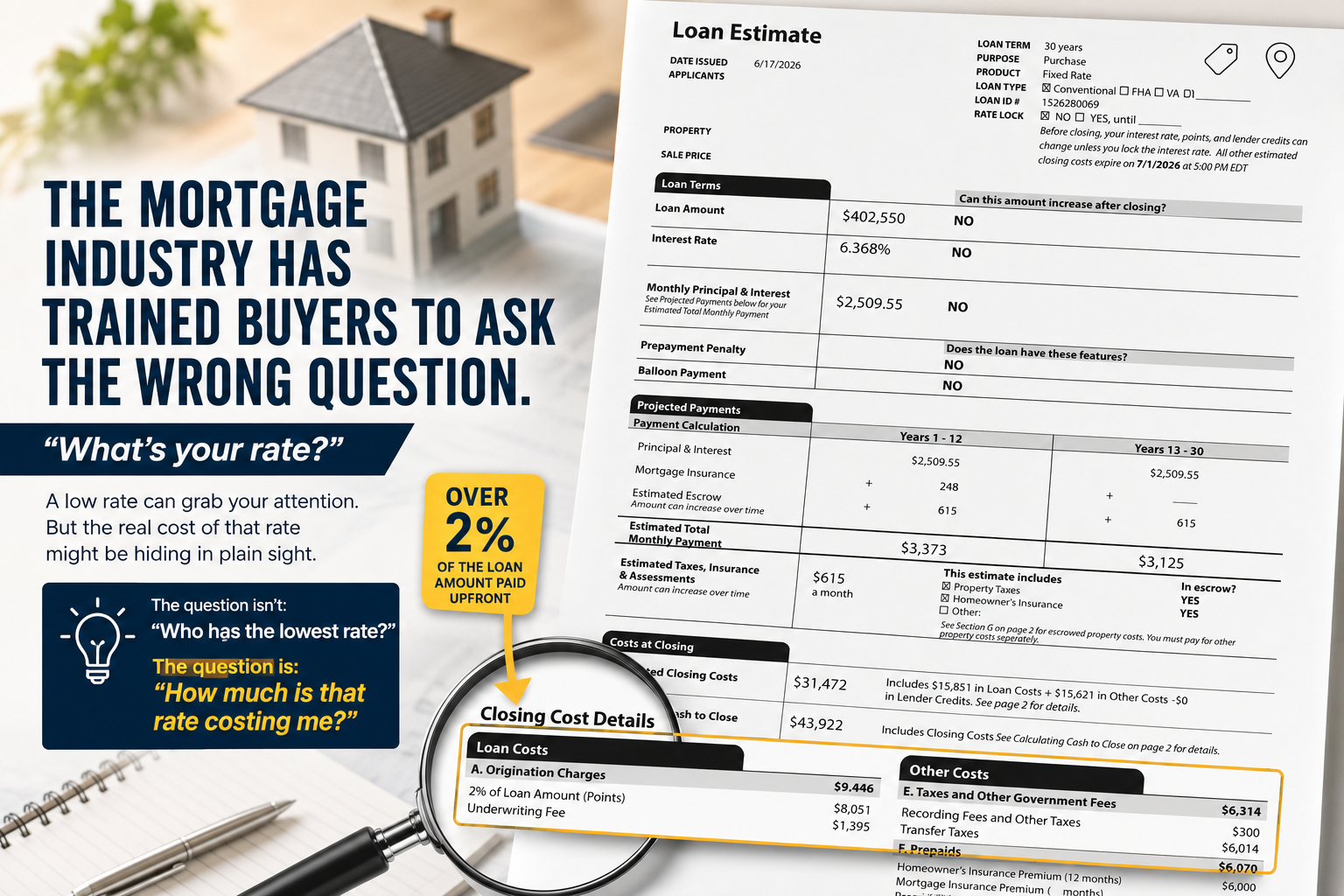

Take the Loan Estimate above as an example.

At first glance, it looks attractive.

A 30-year fixed conventional loan at 6.368%.

Most buyers would stop right there and think:

"That's a pretty good rate."

But the real story isn't in the interest rate.

It's hiding in Box A under Origination Charges.

There you'll find something many buyers never notice until it's too late:

$8,051 in discount points.

On top of that is another $1,395 underwriting fee, bringing total lender charges in Box A to $9,446.

Those discount points are essentially prepaid interest.

You're paying thousands of dollars today in exchange for a lower interest rate over the life of the loan.

Sometimes that's a smart financial decision.

Sometimes it isn't.

The problem is that many buyers never realize they're making that decision.

Why Comparing Interest Rates Can Be Misleading

Imagine two lenders.

Lender A

Interest Rate: 6.37%

Discount Points: $8,051

Lender B

Interest Rate: 6.75%

Discount Points: $0

Which loan is actually better?

The answer depends on several factors.

How long will you own the home?

Will you refinance if rates drop?

Do you have extra cash available today?

How long will it take to recover the upfront cost through lower monthly payments?

If you're planning to move in three or four years, paying thousands upfront may never pay for itself.

If you're planning to stay for twenty years, it might.

There's no universal right answer.

But there is a wrong way to shop...

Choosing solely based on the advertised interest rate.

Ask Better Questions

Instead of asking:

"What's your rate?"

Ask:

How many discount points are included?

Is this rate bought down?

What are my lender fees?

What's the APR?

How long before the lower payment breaks even?

Can you quote this loan with zero points?

Those questions tell you far more than the interest rate alone.

Box A Is Your Friend

Every Loan Estimate issued in the United States follows the same standardized format.

That means you can compare lenders apples-to-apples.

The first place to look is Box A — Origination Charges.

That's where you'll see:

Discount points

Origination fees

Underwriting fees

Other lender charges

It's one of the easiest ways to determine whether a "great rate" is actually costing you thousands more than you expected.

The Bottom Line

Mortgage companies know buyers shop interest rates.

That's why rates often become the headline.

But the smartest buyers look beyond the headline.

They compare the entire loan—not just the number printed in bold.

Because the best mortgage isn't always the one with the lowest rate.

It's the one that costs you the least over the time you actually own the home.